Lets see how many Mondays I do this for…

After last year’s budget within a week many of the announcements were passed into law (in Treasury Laws Amendment (A Tax Plan for the COVID-19 Economic Recovery) Act 2020)

Two of the biggest changes were:

- To allow corporate tax entities with an aggregated turnover of less than $5 billion to carry back a tax loss for the 2019-20, 2020-21 or 2021-22 income year and apply it against tax paid in a previous income year as far back as the 2018-19 income year. Remember that this cannot be done in a way that will put the company’s franking account into deficit.

- To allow businesses with an aggregated turnover of less than $5 billion to deduct the full cost of new depreciating assets that are first held, and first used or installed ready for use for a taxable purpose up to 30 June 2022. Businesses are also able to deduct the full cost of improvements to these assets and to existing eligible depreciating assets made during this period and businesses with an aggregated turnover of less than $50 million can deduct the full cost of second hand depreciating assets that are first held, and first used or installed ready for use for a taxable purpose up to 30 June 2022.

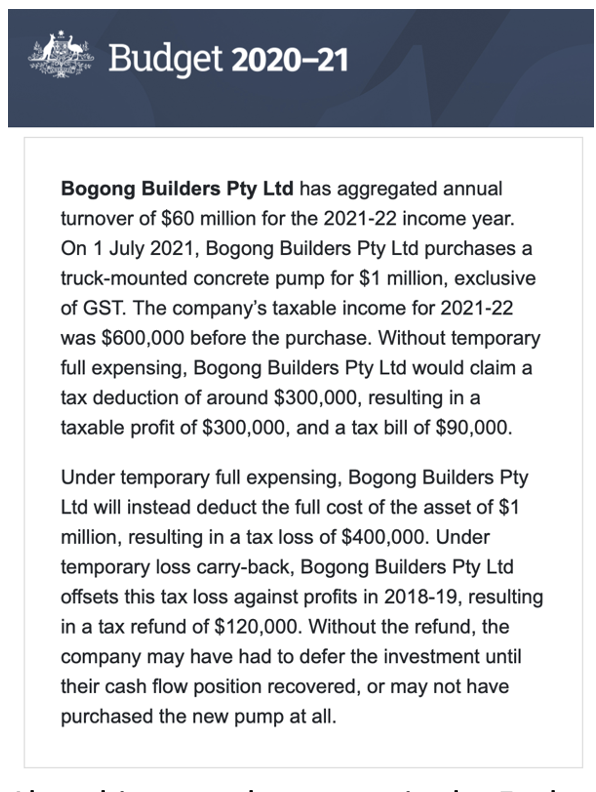

It was pretty clear on budget night that these two announcement might work together, and especially lead to some year-end tax planning ideas. Have a look at this example from the fact sheets released on Budget night back in October.

Also, this example was put in the Explanatory Memorandum to the Bill…

Example 2.2 : Business benefits from temporary full expensing and temporary loss carry back

On 1 November 2021, Company B purchases a truck for $1.5 million. Under the temporary full expensing measure explained in Chapter 8, Company B can deduct the full cost of the truck in the 2021-22 income year. As a result, Company B makes a tax loss of $400,000 for the 2021-22 income year.

In the 2020-21 income year, Company B had taxable income of $8 million. As Company B had an aggregated turnover of $80 million in that income year, it was liable to income tax at the standard corporate tax rate of 30 per cent. Therefore, Company B paid income tax of $2.4 million for that income year. Company B had no net exempt income in that income year.

Company B’s franking account balance at the end of the 2021-22 income year is $1.3 million.

Company B makes a loss carry back choice to carry back the tax loss of $400,000 for the 2021-22 income year to the 2020-21 income year.

The result of the method statement in section 160-10 for the 2020-21 income year is $120,000 – that is, $400,000 x 30 per cent.

As this amount is less than Company B’s income tax liability for the 2020-21 income year ($2.4 million) and its franking account balance for the current year ($1.3 million), Company B’s loss carry back tax offset component for the 2020-21 income year is $120,000.Therefore, when Company B lodges its income tax return for the 2021-22 income year, it will be entitled to a refundable loss carry back tax offset of $120,000.

It is clear that the Government sees that, as we come up to 30 June 2021 and 30 June 2022, we could buy Division 40 assets, get an immediate deduction and get back previous taxes our companies have paid.

Immediate deduction for prepaid expenditure

But there is a third change announced in the same budget and made law in the same Act we need to also consider as we head to the next 30 June and consider year-end tax planning – Being the extension to the immediate deduction for prepaid expenditure.

Small business entities have been able to choose to deduct the full amount of prepaid expenditure relating to a service that will be provided across income years for a period of 12 months or shorter but that ends in the following income year (82KZM ITAA36). But this was extended from 1 July 2020.

Now, from 1 July 2020, a medium business (defined as a businesses that would be a small business entity if the $10 million threshold in the aggregated turnover test were $50 million) is able to also choose to deduct the full amount of prepaid expenditure relating to a service that will be provided across income years for a period of 12 months or shorter but that ends in the following income year.

So we can use this to go further into a loss and get back more of the tax the company paid previously.

But what is the benefit of getting the tax back?

I still think I will use the instant asset deduction and the prepaid expenditure rule to get a company to a taxable income of $0, but I am not sure if I want to use these to take a company into a loss to recover previously paid taxes.

Remember, company tax is really just a withhold tax on resident shareholders as they get the benefit of these taxes under the imputation system when they get a dividend. So in many cases, to solve a Division 7A loan, the company has already paid out the “previously paid taxes” as imputation credits and so there is no tax to carry back any loss to get back.

The question is, what will I do with those previously paid taxes if I done get them refunded to the company? What dividends can I pay out of the company and what imputation credits do I have? Does getting a refund of the tax previously paid just create future unfranked dividends?

I still think a refund is a refund and I will take the opportunity to get the tax back for many companies, but I am sure there will be a few companies where I will find there is little benefit (other than timing) in getting the refund.

Leave a comment