Each year the Commissioner releases a tax determination that encourages drinking. This year it is TD 2021/1 titled “value of goods taken from stock for private use for the 2020-21 income year”.

Back in 2004, the Commissioner released a Practice Statement on valuing goods taken from trading stock for private use by sole traders or partners. It states if you take an item of your business’s trading stock for your private use, you need to account for it as if you had sold it and include the value of the item in your business’s assessable income. To do this a taxpayer should keep records of the actual value of goods they take from their trading stock for their own private use and report that amount

In the Practice Statement the Commissioner states that for certain businesses or industries it is difficult to determine the value of an item of trading stock taken for private use. These businesses and industries include:

- Where there is a transformation process, for example baking

- Where there is a range of small items or ingredients, usually of low value

- That are not suited to inventory systems, or

- That are subject to high turnover, often for cash.

In this case a sole trader or partner can use the amounts the Commissioner provides as estimates of the value of goods taken.

The Commissioner gives an example of how to apply the second of these two options…

Over the income year, Peter Purple the butcher regularly takes home various cuts of meat for his private use. He lives with his wife and a child aged 10.

Peter may account for the items by recording the cost of the items as he takes them and include the total amount as assessable income of the business for that income year.

Alternatively, Peter can use the schedule published by the ATO each year to calculate the total value of items taken and include that total in the assessable income of the business for the income year. If he did this, the amount that he would include should be calculated at the butcher’s rate for 2 adults and one child (16 years or under).

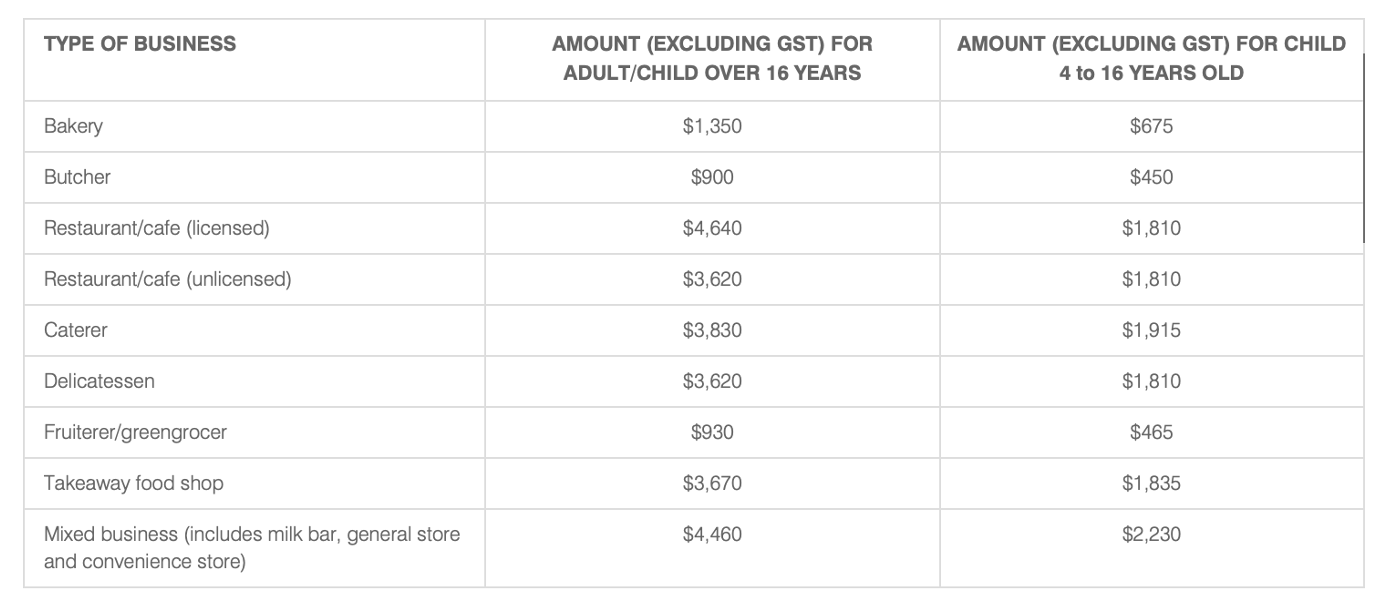

Most people do the first of the two options because of what the yearly determination says is reasonable. Have a look at this year’s table:

If Peter Purple converted his Butcher to a unlicenced café, and took meals home for the family without tracking their actual value, he would be required to add $10,860 to the assessable income of his business.

This outcome drive him to drink, and he gets a liquor licence for his café, which now means he must include an additional $2,040 in his assessable income. Given the average Australian spend $1,500 a year on alcohol, and whether Peter takes one drink or 100 drinks from the café, he still has to include an additional $2,040 in his assessable income, he might as well drink away!

Leave a comment