I do like making life hard for people who ask me basic tax questions. When they ask me if they can claim a tax deduction for a work related expense, I like to say, “based on what I can see, you can’t claim the deduction.” I say that as to be technically correct, if they do not have the required substantiation then there is no deduction.

Even if the work related expense is deductible under section 8-1 of the ITAA97, Division 900 overrides this section and denies the deduction unless the appropriate substantiation is held by the taxpayer.

How the law regarding WRE substantiation works

The rules regarding the required substantiation for work related deductions are found in Division 900 (and Division 28) of the ITAA97.

Division 900 covers substantiation requirements for work expenses (Subdivision 900-B), car expenses (Subdivision 900-C) and business travel expenses (Subdivision 900-D). In this paper, I will limit my discussion to work expenses in Subdivision 900-B (let me know if you want this expanded to cover car and travel expenses).

These substantiation rules only apply to individuals (section 900-5), and only applies to employees or those who have similar withholding as employees (see list in section 900-12).

Section 900-15 states that even if a “work expense” meets the conditions for a deduction (for example section 8-1), there will be no deduction unless the individual substantiates it “by getting written evidence.”

Under section 900-30, a work expense is a loss or outgoing you incur in producing your salary or wages and includes travel and meal allowance expenses, Division 40 deductions and section 25-60, 25-65 and 25-100 deductions.

The written evidence must be retained for 5 years from the due day for lodging an income tax return or when the return is lodged, whichever is later (section 900-25).

There is a “small total of expenses” exception. Subsection 900-35(1) ITAA97 states:

If the total of all the *work expenses (including *laundry expenses, but excluding *travel allowance expenses and *meal allowance expenses) that you want to deduct is $300 or less, you can deduct them without getting written evidence or keeping travel records.

Note that there is an “small total of expenses” equivalent for laundry expenses of $150 under 900-40.

What is written evidence is covered in Subdivision 900-E. It states that written evidence can be a document from the supplier of the goods or services the expense is for. The document must set out:

- the name or business name of the supplier; and

- the amount of the expense, expressed in the currency in which it was incurred; and

- the nature of the goods or services (if the document the supplier gave you does not specify the nature of the goods or services, you may write in the missing details yourself); and

- the day the expense was incurred (if the document does not show the day the expense was incurred, you may use a bank statement or other reasonable, independent evidence that shows when it was paid); and

- the day it is made out.

The hardest part of an employee’s tax return…

Given the pre-filling of income (salary, interest…), private health insurance and other information that is currently available on the tax agent portal and myTax, and given that a large majority of individual taxpayers use tax agents to prepare their tax return, for an individual who predominantly has salary income, substantiating their deductions is the largest regulatory burden, and often the only regulatory burden that the tax system places on them.

This burden involves ensuring they keep invoices from suppliers in relation to these expenses so they can provide them to their tax agent when they are to lodge their tax return. Often, they end up with a bag of invoices only to find out at the end of the process, as the amount that is deductible is less than $300, there was no need to obtain and keep these invoices and they rather could have just kept a list of these expenses.

In addition, as many of these purchases are on line, the individual is not provided with a hard copy invoice and so must save or print off the invoice.

Often invoices are lost or faded and not readable at tax time. In this case the individual may be required to obtain a second copy of the invoice.

The problems of these rules

Problem 1 – 5-year retention period vs 2-year amendment period – Section 900-25

Most employees will only have a two-year amendment period (section 170 ITAA36), but, the current retention period is five years for the substantiation of these expenses (section 900-25).

So three years after your amendment period ended the Commissioner can ask for records for your deductions. I guess this is merely an oversight.

Problem 2 – Small total of expenses less than $300 – Section 900-35

This is the most widely known section of the work related expenses substantiation rules. However, there are two problems associated with it.

The first is that it is, anecdotally, misunderstood. Amongst taxpayer it is often seen as a standard deduction, which it is not, as it is only relief from the requirement to hold certain written evidence of already deductible expenditure.

The second problem, and its main regulatory burden, is that there is no way to know at the time of making a deductible work related expenditure whether this exemption will apply. If I was to purchase a train ticket between two places of work (deductible under section 25-100) on 1 July for $20, I will not know until the following 30 June whether my total claim for work related expenses is $300 or less and so I need to keep an invoice of the travel until this time. It is only after I have collected all the written documentation during the year that I find out at the end of the year that I do not need the written documentation under this section.

This exception from the need to hold written documentation should offer a way to assess what documentation is required at the time of the expenditure not after the end of the year.

How would I do this? Here are my two ideas:

- To replace this yearly exception amount with an exemption for each transaction. Such an exemption currently exists in 900-125 but this only applies to $10 or less amounts, up to a total of $200 and you are still required to make your own written documentation. Examples of this type of documentation exemption exists in other tax acts. In the GST Act, the rules regarding having to have valid tax invoices only apply to expenditure that is greater than $75 (GST exclusive). The concerns about this idea will be expenses can be broken down into components for fall within this threshold. However, we have “set” rules in Division 40 regarding the instant assets for non-business entities where the asset is less that could be used to fix this problem (see subsection 40-80(2))

- Allowing an individual employee to not obtain written documentation for their first $300 (or other appropriate amount) of expenditure. This would still require them to know what they have already spent in a year to assess if they need to keep/obtain documentation so is not as simple as the first option.

Problem 3 – The use of on-line bank statements and other records…

In Practice Statement Law Administration PSLA 2005/7 (as updated to July 2015), the Commissioner states:

Where the above documents are insufficient, we accept the following documents (or combinations of documents) as acceptable evidence of expenses:

- bank statements

- credit card statements

- BPAY reference numbers, combined with bank statements, or

- BPAY reference numbers, combined with tax invoices.

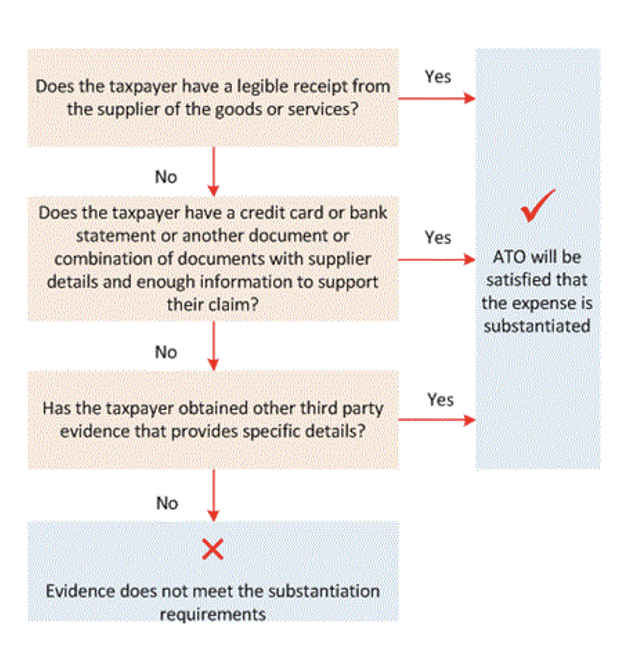

The Practice Statement has the following diagram:

Subdivision 900-E states that “written evidence” must be “a document from the supplier of the goods or services the expense is for” (see subsection 900-115(2)). However, the second square in the document above shows that the Commissioner may accept merely a credit card or a bank statement. Further, subsection 900-115(3) states that if the written evidence from the supplier does not contain all the information required an individual can either use a “bank statement” or write the information themselves. But how do you “write” information on an electronic bank statement from an app on your phone?

Finally, under section 900-125, if an expense is $10 or less, and you have a small total of small expenses (less than $200), you can make a record of the expenses instead of getting a document from the supplier.

All this goes to show that in many cases, the law and the practice of the Commissioner is not to require documentation from the supplier, but rather is to allow the individual to substantiate their work related expense through bank statement, credit card statement, and even through their own documentation. But importantly, in most cases this will not be enough.

Given the rise of electronic commerce, and the ability for tracking expenses in bank apps, you do wonder when the Commissioner might start accepting this as evidence of a deductible expense.

The lessons

- Work related expense are not deductible if they are not substantiated with the right information.

- A bank statement on its own will almost never be enough as it does not have…

the nature of the goods or services (if the document the supplier gave you does not specify the nature of the goods or services, you may write in the missing details yourself); and

- You need to keep this documentation for 5 years.

- To work out how much of the $300 record keeping exemption you can claim, you need some form of records to work out what was spent.

- Electronic bank accounts will not be enough and you should be taking photos of invoices for WRE.

Leave a comment