Back on 1 July 2017 we all became experts on the $1.6 million transfer balance cap. The only amount that we could transfer into a tax free retirement phase was $1.6 million.

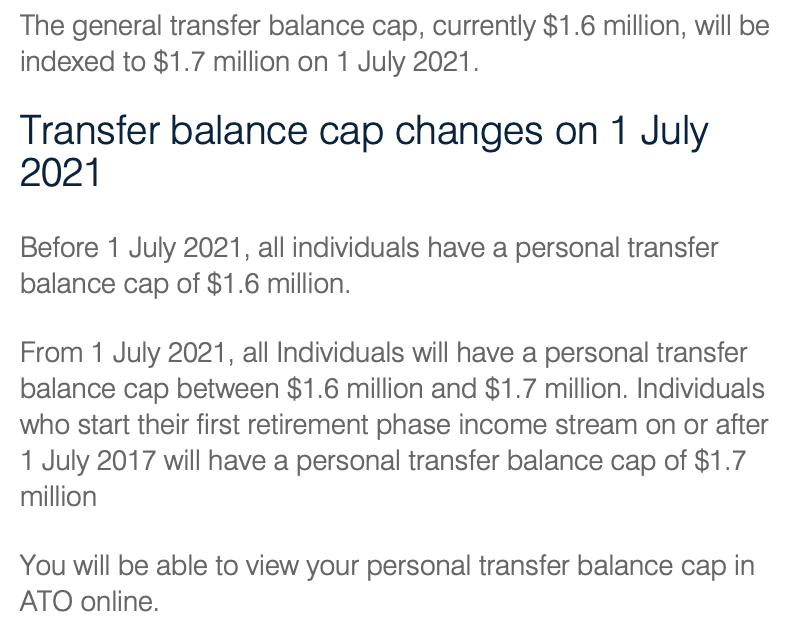

But now the Commissioner has just told us that the “superannuation general transfer balance cap” will increase from $1.6m to $1.7m on 1 July 2021.

That seems easy, but don’t be fooled. Get ready to have a headache…

It starts off pretty easy… If you start your first a “retirement phase superannuation income stream” after 1 July 2021, then you can transfer $1.7 million into the fund to support it.

Now it gets a bit harder… If you started your first a “retirement phase superannuation income stream” before 1 July 2021, and you transferred $1.6 million into the fund to support it before 1 July 2021, even though the cap goes to $1.7 million on 1 July 2021, you can’t add in another $100,000. As you used 100% of the cap that applied when you first started the retirement phase superannuation income stream, you are not allowed to add anything more – you have used 100% of the cap.

Planning idea #1… If you wait until 1 July 2021 to start the retirement phase superannuation income stream you can put an extra $100,000 in to support it.

And now the headache starts… What happens if you started your first a “retirement phase superannuation income stream” before 1 July 2021, but you transferred less than $1.6 million into the fund to support it? For example, what if you transferred $960,000 on 1 January 2020 – How much more can we contribute after 30 June 2021?

First, we need to work out what percentage of the cap we used when we transferred the $960,000 on 1 January 2020. $960,000 divided by $1.6 million is 60%, so we used up 60% of the cap and so we still have another 40% we can use later.

On 1 July 2021, with the transfer balance cap going to $1.7 million, and having 40% of the cap available, we can now transfer in 40% of $1.7 million – or $680,000.

That means to completely use up the transfer balance cap we transferred $960,000 on 1 January 2020 and $680,000 on 1 July 2021, for a total of $1.64 million.

Good luck getting this right every time.

It is worth noting that the above is the way I think it is best to understand what has to be done, but the legislation gets to the same outcome another, less intuitive way. The legislation states first you identify the highest ever balance in your transfer balance account ($960,000 in the example above), then use this to work out the unused cap percentage of the transfer balance account (in the example above 40%). You multiply this percentage by $100,000 ($40,000 from the example above) and add this to $1.6 million to get the new Transfer Balance Cap ($1.64 million).

How this changes the defined benefit income cap

The defined benefit income cap, which is just the general transfer balance cap divided by 16, increases from $100,000 to $106,250 from 1 July 2021. Therefore, the amount of defined benefit income that can be exempt from tax increases each year by $6,250.

How this changes non-concessional contributions

The limit on non-concessional contributions increases to $1.7 million on 1 July 2021. This means that individuals with a total superannuation balance of $1.7 million or more on 30 June 2021, will not be able to make any contributions.

Planning idea #2… Everyone who has made $1.6 million of non-concessional contributions and is not in retirement phase yet can now make another non-concessional contribution of up to $100,000 from 1 July 2021.

And yes I know it is a Sunday and not a Monday… but I am bored…

Leave a comment