What is the Company Tax Rate?

This once was an easy question. Only a few years ago the answer was easy… 30%. But recently there have been numerous changes to the company tax rate.

In addition to the 30% tax rate we now have a lower rate, which is…

Year BRE tax rate (%)

2017-18 27.5

2018-19 27.5

2019-20 27.5

2020-21 26.0

2021-22 onwards 25.0

Note that company tax, where all profits are paid out as a dividend, is just a withholding tax on shareholders. The tax rate makes a difference when there are non-resident shareholders or investments and assets purchased in the company.

What is a base rate entity?

From 1 July 2017, the lower corporate tax rate would only apply to any corporate tax entity that is a “base rate entity”.

A base rate entity is a corporate tax entity that meets a turnover threshold. The turnover threshold is an aggregated turnover of less than $50 million.

Aggregated turnover is defined as (subsection 328-115(2) ITAA 1997)

- your annual turnover for the income year; and

- the annual turnover for the income year of any entity (a relevant entity) that is *connected with you at any time during the income year; and

- the annual turnover for the income year of any entity (a relevant entity) that is an affiliate of yours at any time during the income year.

Also, for a company to qualify as a base rate entity it must pass a passive income test.

Under the passive income test, companies that are generating predominantly passive income will not be eligible for the lower corporate tax rate.

Therefore, a company will qualify for the lower corporate tax rate for an income year only if:

- no more than 80% of the company’s assessable income for that income year is base rate entity passive income; and

- the aggregated turnover is less than the aggregated turnover threshold for that income year.

80% passive income test

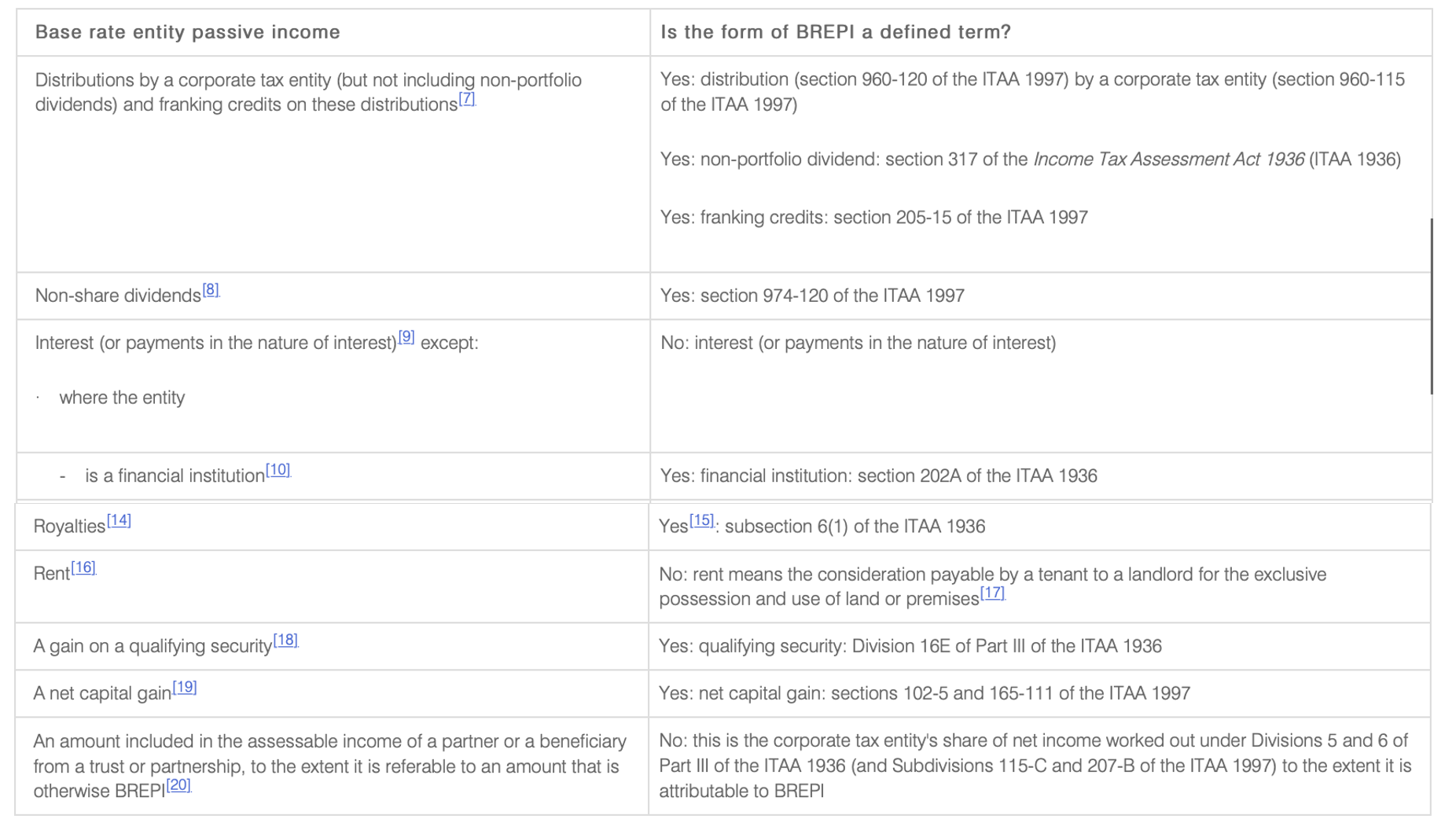

An amount is base rate entity passive income if it is:

- A distribution or dividend by a corporate tax entity, other than a non-portfolio dividend;

- Franking credits attached to such a distribution or dividend;

- A non-share dividend made by a company;

- Interest income;

- A royalty;

- Rent;

- A gain on a qualifying security; or

- A net capital gain.

Also, an amount that flows through a trust to a corporate tax entity will retain its character for the purposes of determining whether or not the amount is base rate entity passive income of the corporate tax entity.

For example, a dividend which passes directly from the trust to a beneficiary that is a corporate tax entity will be base rate entity passive income of the corporate tax entity because the trust distribution is directly referable to the dividend of the trust.

Example

Jane and Dave Smith are the sole shareholders and directors of Smith Pty Ltd. Smith Pty Ltd holds a diversified portfolio of shares from which it earns dividend income as well as several term deposits from which it earns interest. It is also the beneficiary of a trust which owns a commercial investment property. All rental income earned by the trust is distributed to Smith Pty Ltd.

Smith Pty Ltd also earns a small amount of fee for service income. This is derived from the consulting services Jane Smith, a retired business woman, provides to a number of independent businesses year.

In the 2017-18 income year, Smith Pty Ltd had an aggregated turnover that is under the $25 million aggregated turnover threshold. The amount of its assessable income was $900,000, comprising:

- dividends, rent and interest income of $620,000;

- net capital gains of $180,000; and

- consulting income of $100,000.

Smith Pty Ltd is a passive investment company as 89 per cent of its assessable income is base rate entity passive income. Consequently, for the 2017-18 income year, Smith Pty Ltd’s corporate tax rate is 30 per cent.

The Commissioner’s guidance on base rate entities can be found at LCR 2019/5. In it is the following helpful table…

Let’s just note a couple of tricks people make:

- Rent is always Base Rate Passive Income so if you run a business of renting out commercial offices/spaces you will almost certainly have a company tax rate of 30%. The companies that rent out your commercial offices will most likely get the lower rate. Does not seem fair!

- A non-portfolio dividend is not Base Rate Passive Income. So if the company receiving the dividend owns 10+% of the company paying the dividend then it is not Base Rate Passive Income. But if a trust owns the shares of the dividend paying company, and another company is made presently entitled to the dividend this will be Base Rate Passive Income as the second company does not own 10% of the shares of the first company (because the trust owns the shares).

Example

Company 1, Sub Trust 1 and Bob are beneficiaries of the Busy Trust. The net income of Busy Trust consisted of the following amounts:

- $500,000 business income (net of expenses)

- $300,000 unfranked dividend (net of expenses), and

- $200,000 rental income (net of expenses).

For trust law purposes, the trustee of Busy Trust resolved to make Company 1 presently entitled to its net business income, Bob presently entitled to the net unfranked dividend and Sub Trust 1 presently entitled to the net rental income.

For tax law purposes, as Company 1 was presently entitled to $500,000 of the trust’s income available for distribution (that is, $1 million or 50%), it was assessable on 50% of the trust’s net income.

Although Company 1’s share of net income is $500,000, that amount is not referable solely to business income. The effect of Division 6 of the ITAA 1936 is that Company 1’s share of net income is attributable to:

- $250,000 of business income, which is not BREPI

- $150,000 of unfranked dividend income, which is BREPI, and $100,000 of rental income, which is BREPI.

Assuming Company 1 has no other income, its BREPI will be 50% of its assessable income.

Leave a comment