I am always getting asked about bonuses, and generally it is around the timing idea of declaring the bonuses before 30 June so the employer gets the deduction in year 1, but paying the bonus after 30 June so the employee has to pay tax in year 2. Yes, you can do this…

But I have always wondered if I should say that bonuses might not be the best way to reward employees.

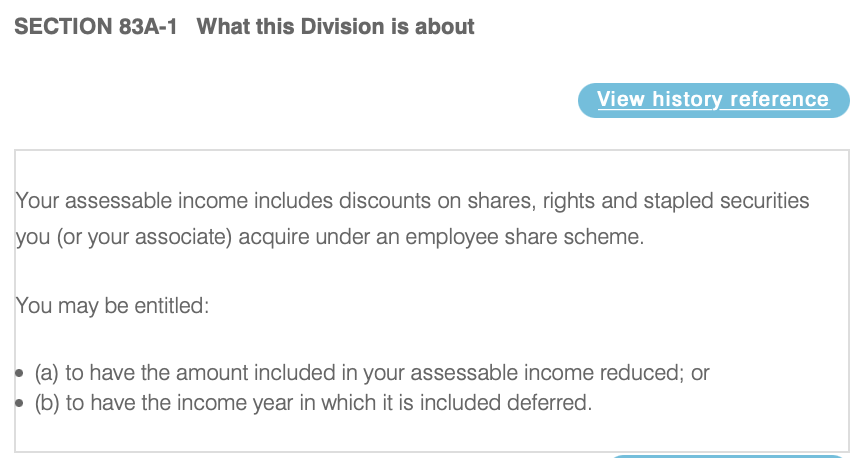

In Division 83A of the ITAA are three concessional tax treatments or employee share schemes. One is for “Start-up” companies, one defers tax till a later date, but the third is the concession I have always been tempted to raise.

This concession, called the “Taxed-upfront scheme – $1,000 reduction” by the Commissioner, allows employers to give/issue shares to employees at a discount to their market value, and the amount that is taxable is the discount less $1,000.

If you give me a $1,000 bonus, I get taxed on the $1,000. However, if you give me $1,000 of shares, subject to certain conditions, I pay no tax at all.

What are the conditions?

For an employee to be able to reduce the discount amount (that otherwise must be included in their taxable income) by up to $1,000, all of the following conditions must be met:

- The ESS interests (either the share or the option) provided to employees must be in a company or a holding company;

- The employer is not a share trading company;

- The shares or the options to buy shares must be ordinary shares;

- This arrangement does not result in any employee (or their associates) owning more than 10% of the company;

- There must be no real risk of forfeiting the share or the option;

- The employee’s adjusted taxable income (ATI) for the income year must be $180,000 or less;

- The scheme must be offered to at least 75% of the Australian-resident permanent employees with at least three years’ service; and

- The scheme must be operated so that the employees must hold their shares or options for a minimum of either three years, or until their employee ceases employment.

After a good year, you want to give all your employees a big thank you. And to save them tax you give them all $1,000 of shares that they can sell in 3 years (or if they leave) and they pay no tax on it (other than any CGT when they sell it but with a $1,000 cost base).

But doesn’t the employer miss out on the deduction they would have got if they paid a bonus?

Good question, as generally when a company issues shares or rights they do not get a deduction.

However, if an employer issues share or options under this “reduction concession”, they can claim a tax deduction equal to the discount given, up to a maximum of $1,000 for each employee.

Importantly, the employer still gets the deduction if the employee has an ATI above than $180,000 and so has to pay tax on the total discount.

Leave a comment