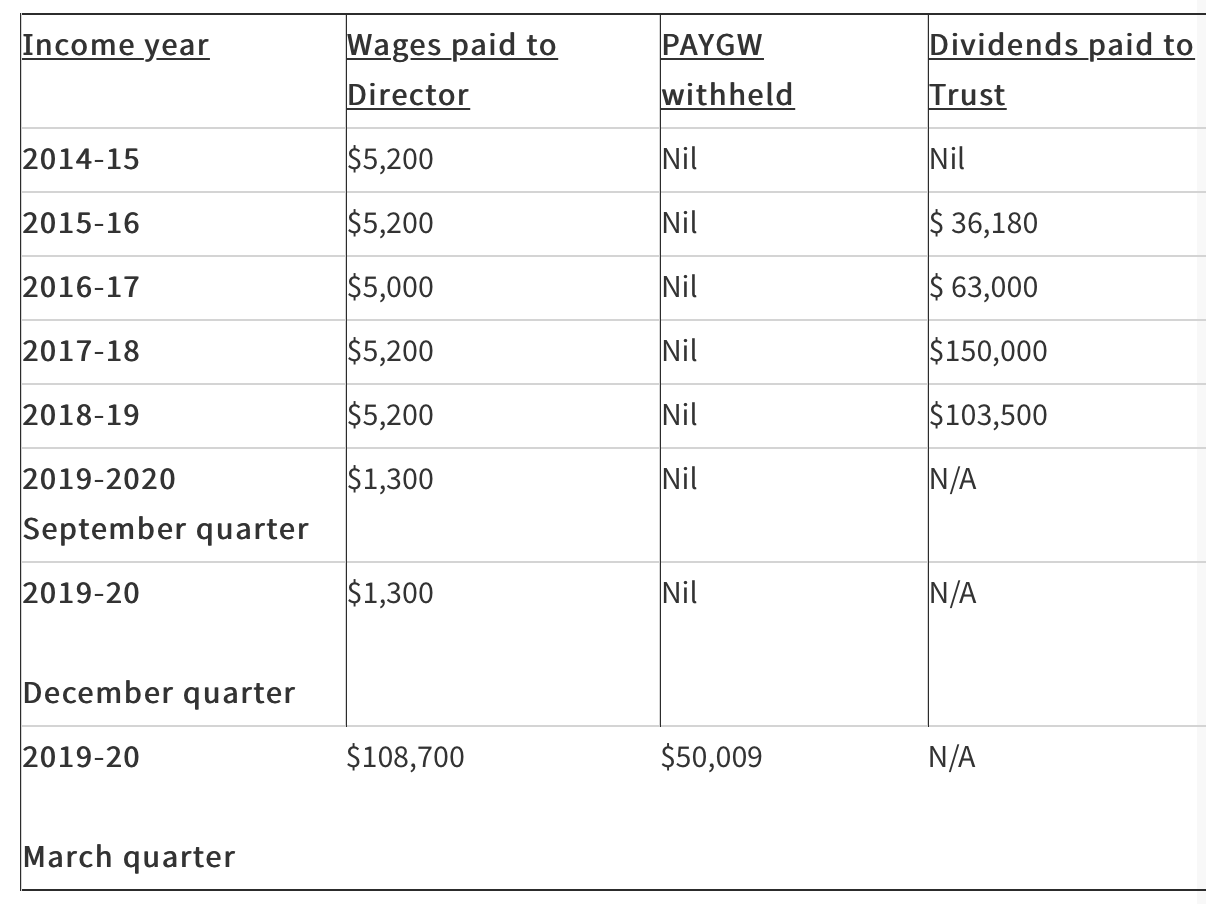

In the case of VNBM and Commissioner of Taxation [2021] AATA 1626 the directors of a company made the following payments…

So why would the directors (spouses with the husband being an accountant and tax agent) decided to pay such a large salary in the March 2020 quarter? Have a look at the PAYGW for that quarter o just over $50k and remember what the limit of the Cashflow Boost was…

The Commissioner applied the rules in the Cashflow Boost that deny the payment where there has been a scheme for the sole or dominant purpose to get the payment.

The director said he only made the increase in salary after a discussion with his bank who suggested they look more favourably on salary… but the bank had no record of such a statement.

Seven months after the Commissioner first raised concerns about the increased salary in this quarter the director “found” a minute from the period resolving to make the payment. The AAT suggested this may not have been created on the date it was signed but may have been created much later.

And just to top this off, no payment was actually made to the director. The director argued that there was money in an account that was earmarked to be paid and that should be enough…

The AAT rightly said, no Cashflow Boost for this taxpayer.

Leave a comment