Most Division 7A loans are repaid without a single bank transaction. They are typically made by way of set-off against a dividend declared by the company. But what are the requirements we need to follow to make these set offs legal?

Some people say that we do a journal that creates a dividend that equals the required minimum yearly repayment and then offset it against that repayment. But remember a journal does not create anything, rather it records what happened, and if what the journal says happened did not happen, the journal is wrong. (paragraph 6 of miscellaneous tax ruling MT 2050)

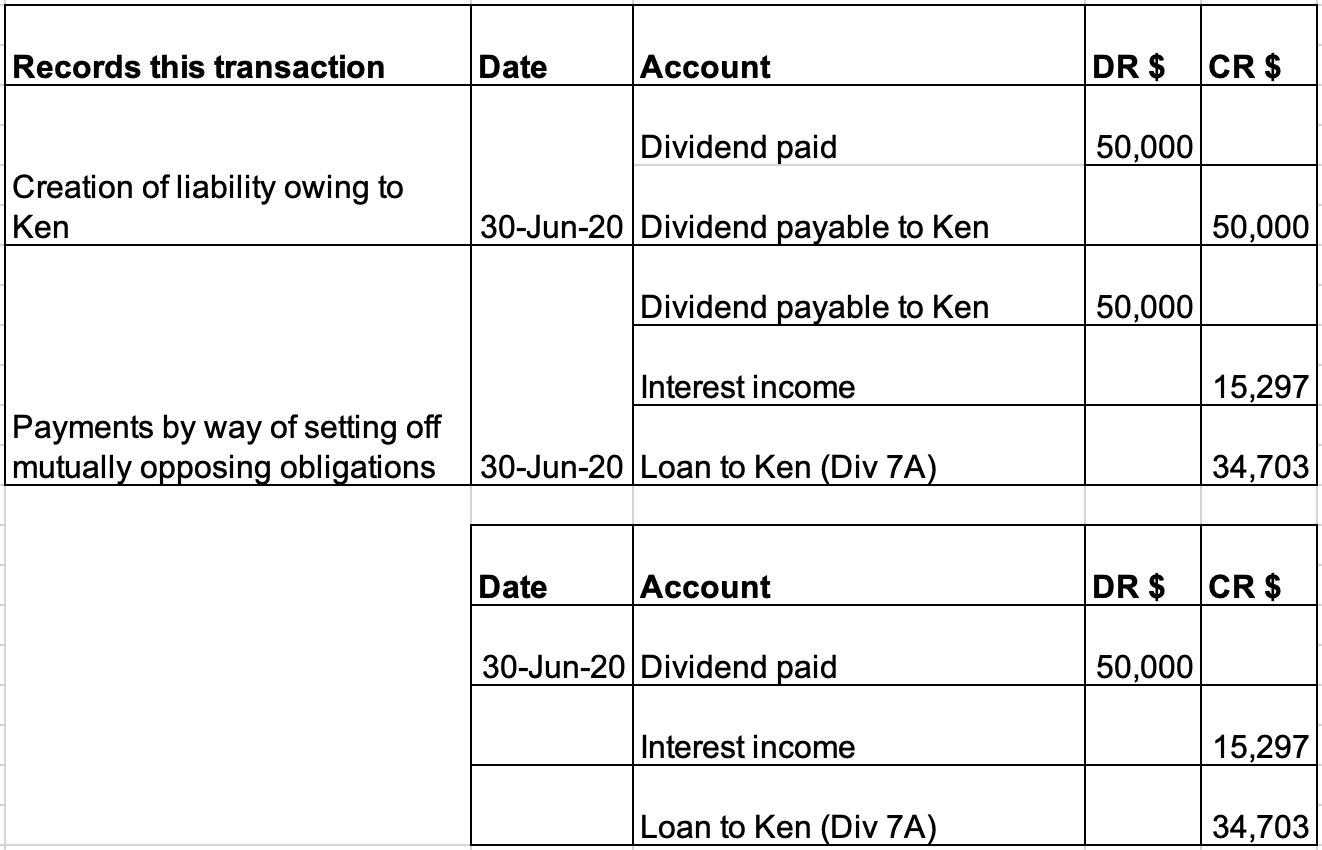

Let’s look at the following example and journals, and see what we need to do legally to make it occur…

But now comes the most important question… Do these journals represent the reality of what actually happened?

Was there an actual dividend ?

A dividend cannot be created by journal but must be declared in accordance with the company’s constitution and the Corporations Act 2001. This is done by a Board resolution at a meeting of directors. And for the dividend to be in existence at 30 June to offset against the minimum yearly repayment the meeting and resolution has to be done by 30 June. If there was no meeting and no resolution there was no dividend and no minimum yearly repayment was made!

How do we prove this happened by 30 June? Under section 251A of the Corporations Act minutes must be filed in the company register within one month, so for a resolution on 30 June 2020 the minute must be filed in the company register by 30 July 2020.

What happens if we file minutes after the one-month deadline?

First there is a penalty of $6,660 per offence (but this is never enforced). But more importantly, the minutes are prima facie evidence of the dividend being paid. If they lodged after the required time they are not evidence of the dividend and the Commissioner can ask the directors if they remember the meeting on 30 June when they declared the dividend (possibly while they were hiking in uncontactable jungles). I have no examples of this occurring.

Distribution statements

Subdivision 202-E states that a private company has 4 months after their year end to provide Distribution Statements to shareholders, so by 31 October after year end.

Interestingly, as distribution statements are not required to be signed by anyone, there is not written evidence of when it was provided to the shareholder… But if this is not provided within four months after the year end, a first offence of giving a distribution statement late is punishable by a fine of up $4,440 (but to get this the Commissioner has to instigate a court process so it is very unlikely). Most importantly, providing it late does not cause the dividend declaration to be invalid.

Are your journal paid minimum yearly repayments legal

Did the Board meet and resolve to pay the dividend equal to the minimum yearly repayment by 30 June? Where the minutes put in the corporate register by 30 July? Where distribution statements done by 31 October?

Its not like the Commissioner has made this an issue, but at least you know know your client’s risk.

Leave a comment