In December 2017 the Commissioner stated he was going to suspend guidelines on alienating profits from firms. He indicated that early in 2018 he would release new guidelines… and in December 2021 he has not reissued these guidelines.

These guidelines cover arrangements where:

- taxpayers redirect their income from a business or activity to an associated entity;

- that income includes income from their professional services; and

- the outcome is that they significantly reduce their tax liability.

The new guideline (PCG 2021/4) applies from 1 July 2022… But…

If you have existing arrangements, you can continue to rely on the suspended guidelines for 1 July 2017 to 30 June 2022 if your arrangement is commercially driven and does not exhibit any of the high-risk factors listed below.

More importantly, if you find that an arrangement was low risk under the suspended guidelines but has a higher risk rating under PCG 2021/4, you can continue to apply the suspended guidelines until 30 June 2024!!!!!

A summary of the suspended guidelines we can use to 30 June 2024

The suspended guidelines were much simpler than what you will see below. They were that if any of three benchmarks were satisfied, then the practitioner would be considered low risk and unlikely to be subject to ATO review provided no other compliance issues were evident.

The three benchmarks were:

- The income derived by the professional practitioner had to be at least the level of remuneration paid to the highest band of professional employees providing equivalent services to the firm. If the firm did not have any employees providing equivalent services, you could use data from comparable firms or industry benchmarks

- The income derived by the professional practitioner had to be at least 50% of the firm’s income to which the practitioner and their associated entities were collectively entitled

- The practitioner and their associated entities both had to have an effective tax rate of 30% or higher on the income received from the firm

Give the professional 50% of the income from the firm and send the other 50% to the spouse, adult kids, other entities… and there was no risk. Pay them a commercial rate and there was no risk…

This is probably what we will use until 2024, but then we will be stuck with the new guideline.

The new guidelines in PCG 2021/4

First issue – pass two “gateways”

The Guideline states that first we must assess if our arrangement is commercial and does not have high-risk features.

The first is we need to pass through the commercial rationale gateway, by showing the arrangement is commercial. The Commissioner states the following arrangements show a lack of commercial rationale:

- seem more complex than necessary to achieve the relevant commercial objective

- appear to serve no real purpose other than to gain a tax advantage

- have a tax result that appears to be at odds with its commercial or economic result

- result in little or no risk in circumstances where significant risks would normally be expected

- operate on non-commercial terms or in a non-arm’s length manner

- present a gap between the substance of what is being achieved and the legal form it takes.

The second gateway is the “no high-risk features” gateway. The Commissioner states that arrangements with high-risk features can:

- have financing arrangements relating to non-arm’s length transactions

- exploit the difference between accounting standards and tax law

- be materially different in principle from Everett and Galland

- involve multiple classes of shares and units, including creating discretionary entitlements such as dividend access shares

- involve multiple assignments or disposals of an equity interest

- misuse the superannuation system, including assignments or disposals of an interest to associated SMSFs

- distribute income to entities with losses.

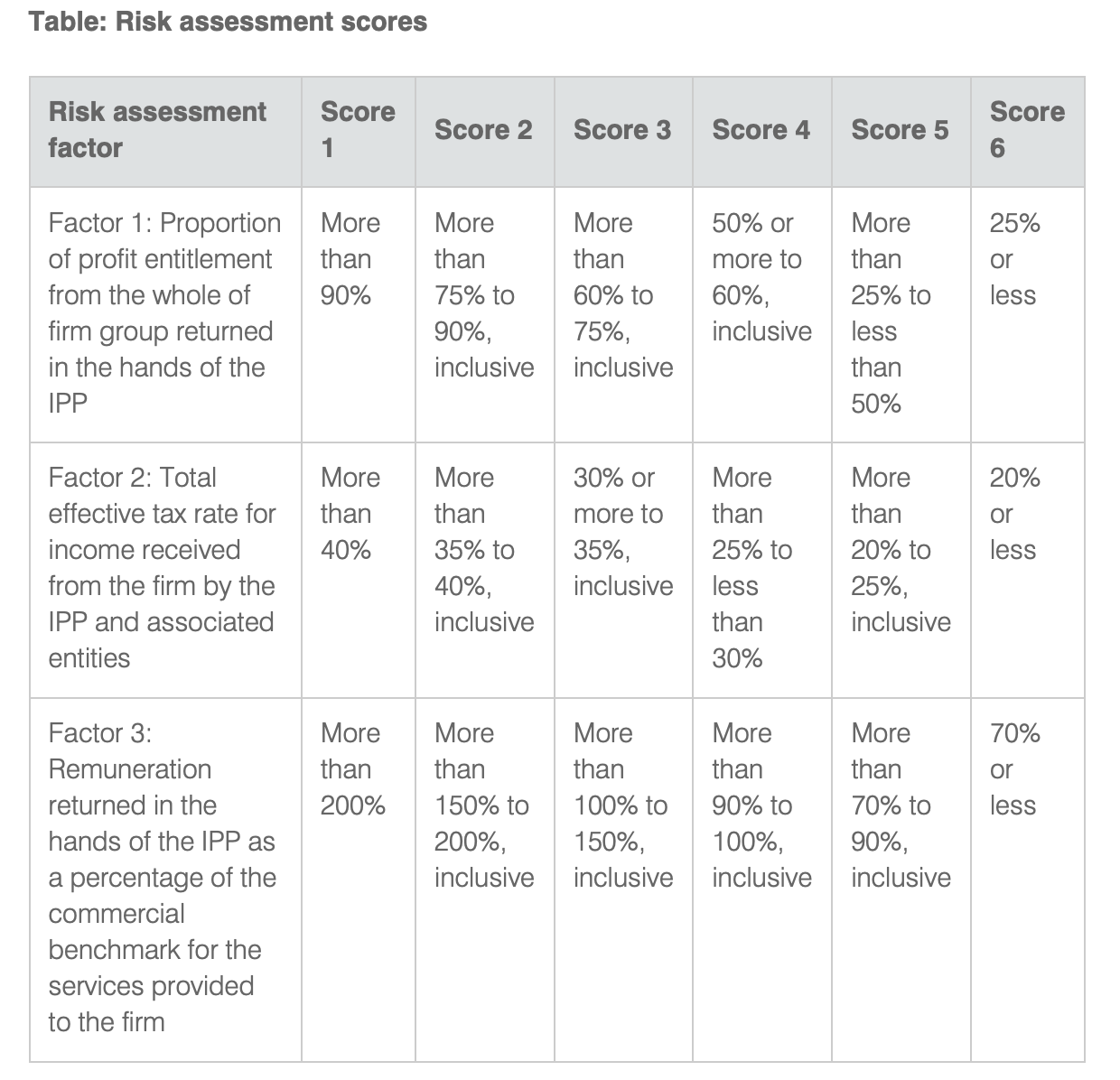

Risk Assessment Framework

If you do pass both gateways, you can then self-assess against the Risk assessment framework to see the type of compliance attention that we will give to your arrangement.

This involves testing the arrangement in three ways (or just two ways if the third test does not make sense) and adding up the “risk points” from the table below.

For example, if the partner in the engineering firm took 62% of the amounts coming from the firm (Factor 1 is score 3), the effective tax rate across all of the income coming out of the firms was 28% (Factor 2 is score 4) and there is no commercial benchmark (Factor 3 does not apply, the risk score is 7 (3 + 4) and this in the table below say we are at low risk.

Have a look at one of the Commissioner’s examples

Julie and 3 other individuals run a legal practice through Legal Services Pty Ltd. Julie’s family trust, JJ Trust, is a shareholder in the company. The beneficiaries of JJ Trust include Julie, her spouse Kurt and a corporate beneficiary, Company X Pty Ltd, whose shares are held by Julie.

Julie’s total income entitlement from the company, which includes her salary and wages and franked dividends to her family trust, is $800,000. She includes $380,000 received as salary and wages from the company in her tax return. She reflects this is an appropriate return for her services she provides. The tax paid on this amount is $141,667.

The trustee of the JJ Trust receives $420,000 as a fully franked dividend ($294,000 as cash and $126,000 as franking credits). The trustee distributes:

- $370,000 to the corporate beneficiary Company X Pty Ltd; and the tax paid on this amount is $96,200 (applying 2020–21 company tax rate of 26%)

- $50,000 to Julie’s spouse, Kurt; and tax on this amount is $6,717 (applying 2020–21 individual tax rates).

The total tax paid by Julie and her associates is $244,584 ($141,667 + $96,200 +$6,717). This gives a total effective tax rate of 30.57% ($244,584 ÷ $800,000 × 100). This arrangement is considered moderate risk as Julie:

- returns 47.5% of her profit entitlement from the partnership in her personal tax return, which gives her a risk score of 5 against the first risk assessment factor

- and her associates pay an effective tax of more than 30% on the income received from the partnership, which gives her a score of 3 against the second risk assessment factor

- has determined the appropriate commercial remuneration to benchmark her remuneration against for the services she provides to the firm

- The industry benchmark for the provision of equivalent or similar services is $325,000.

- As she personally returns $380,000 (which is 116.9% of the benchmark remuneration ($380,000 ÷ $325,000 × 100)), this gives her a score of 3 for the third risk assessment factor.

Julie’s total score against the 3 risk assessment factors is 11, which places her arrangement in the moderate risk category.

Questions I am sure I will get asked

Ken, what if we also get related service trust income? Add it in to the total calculation for Factor 1 and Factor 2.

Ken, what if I have rental loses or other deductions? For the purposes of calculating the total effective tax rate in Factor 2, deductions not related to the professional income are disregarded.

What if I am Amber or Red? If you find your client is Amber, the Commissioner states “We are likely to conduct further analysis on the facts and circumstances of your arrangement. We may contact you to understand the arrangement and resolve any areas of difference.” If you find your client is Red, the Commissioner states “We will conduct further analysis on the facts and circumstances of your arrangement as a matter of priority. If further analysis confirms the facts and circumstances of your arrangement remain high risk, we may proceed to audit where appropriate.” So you will want to stay GREEN.

What does this mean for us?

- Stick with the old rules until 2024

- From 1 July 2024 we will have to play with how much we give to other associated entities to get a low risk, possibly only giving them much less than 50% as we could under the suspended guidelines

- I imagine we will be looking for high “commercial benchmark rates” (Factor 3) as a way to bring down our risk rating. If you can show your client is being paid 200%+ of the commercial benchmark for the services they provide to the firm that gives you 9 risk points to play with for Factors 1 & 2

Leave a comment