Since 1978 there has been a scary anti avoidance provision in the back of the trust tax rules in the ITAA36 called “reimbursement agreements” that the Commissioner has generally ignored…

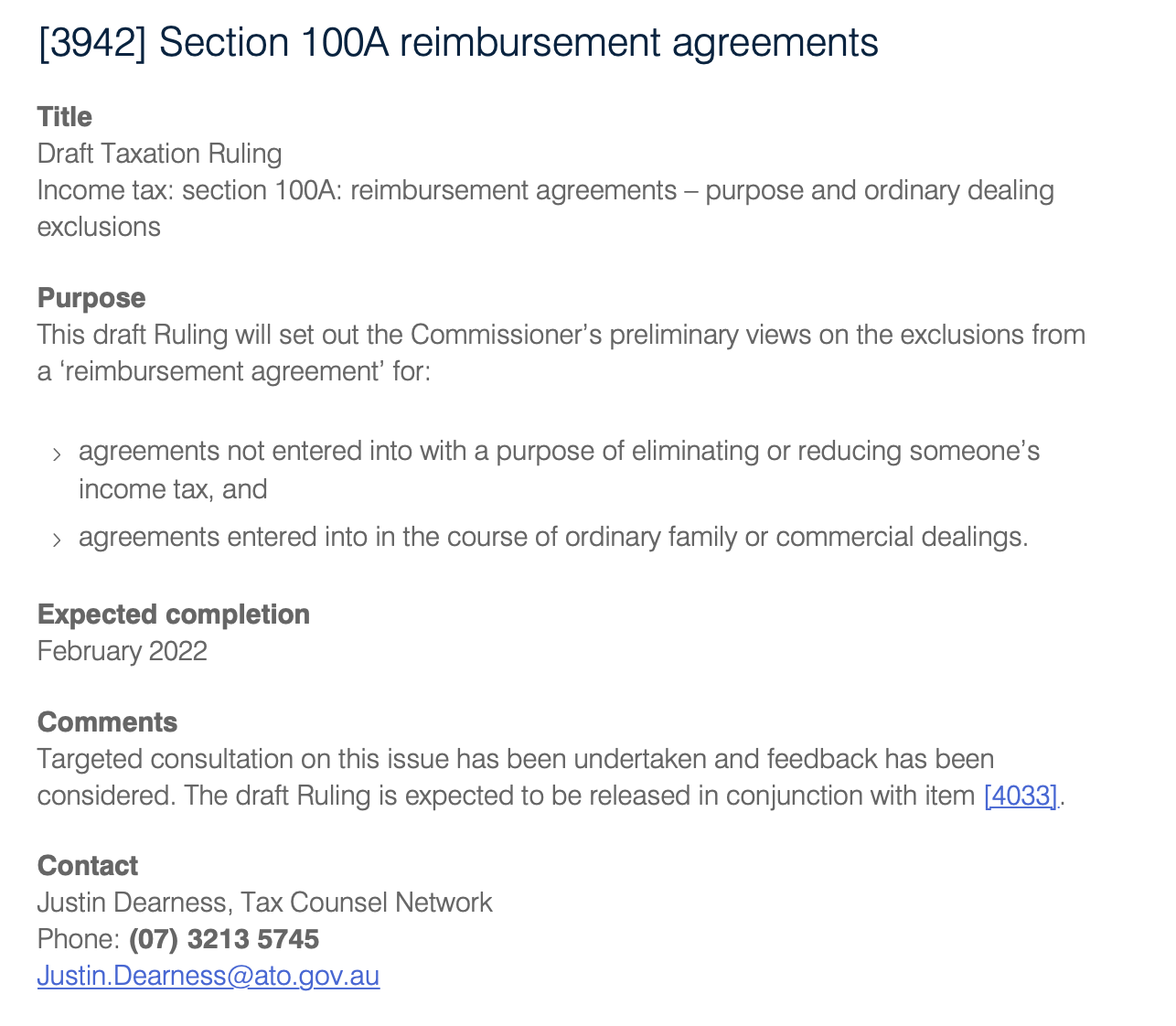

What makes it even scarier is in February 2022 the Commissioner is about to start using this section (100A) and his first offensive will be a new Taxation Ruling (see below) and the rumour is he is going to stop standard practices under this Ruling (like giving a kid $416 but not actually giving the kid the cash)

But, just before he started this offensive, the Federal Court has decided these rules do not apply in a common situation. Hopefully it will blunt his attack!

Question 1 – What is a 100A reimbursement agreement?

Section 100A of the Income Tax Assessment Act 1936 states that, to the extent a trust beneficiary’s entitlement arises out of a reimbursement agreement, then the entitlement is disregarded and the trustee pays tax on it at the highest marginal rate.

A reimbursement agreement generally involves making someone presently entitled to trust income in circumstances where both someone other than the presently entitled beneficiary actually benefits from that income, and at least one party enters into the agreement for purposes that include getting a tax benefit. An example could be…

The trustee of a trust estate makes a beneficiary entitled to trust income. Instead of paying the amount of trust income to the beneficiary, the trustee gives, or lends on interest-free terms, the money to another person. The other person benefits from the trust income, but is not assessed on any part of it. This arrangement would generally constitute a reimbursement agreement if it was intended that the beneficiary who was made presently entitled to the trust income pays a lower amount of tax (lower tax rate, losses, tax-exempt, deductions) than would have been payable by the person who actually enjoyed the economic benefits of that income.

However, section 100A doesn’t apply where an agreement has been entered into in the course of an ordinary family or commercial dealing. This has been the reason the Commissioner has not been able to use this section, but the rumour is he will very much limit what this means in the February ruling.

Question 2: What did the Federal Court case state?

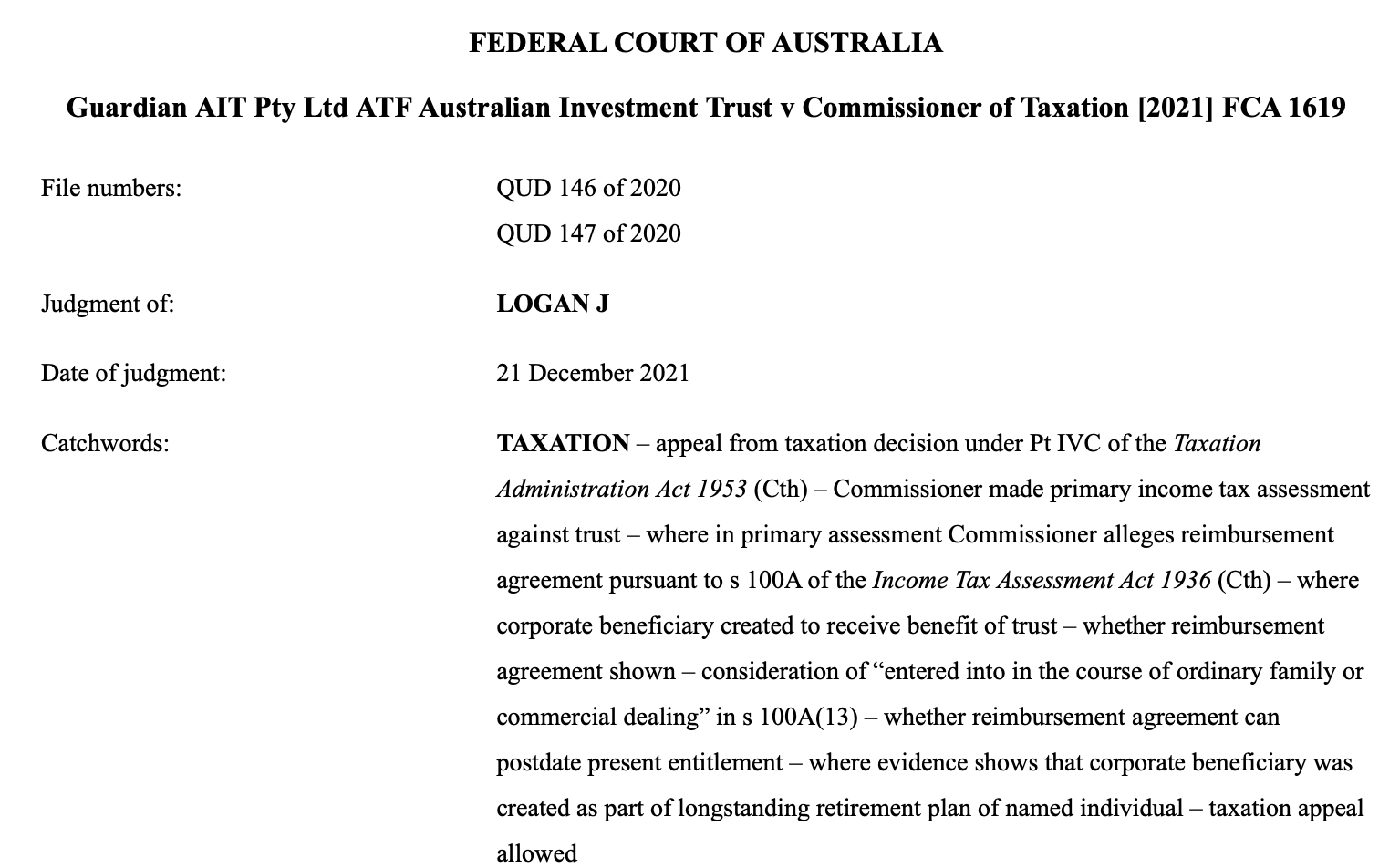

Guardian AIT Pty Ltd ATF Australian Investment Trust v Commissioner of Taxation [2021] FCA 1619

The facts in this case are that there were distributions of income by a trust to a corporate beneficiary, and then the amount was returned to the trust by dividends. This was then held on trust for the owner of all the entities.

This was not a reimbursement agreement as each step was separate and not part of the same agreement – the addition of the corporate beneficiary and making it presently entitled to income of the trust was NOT related to a later decision to pay the dividend. The Court also decided the arrangement was part of ordinary family or commercial dealings.

The Court concluded that the appointment of a “clean skin” company as a beneficiary was done as a risk minimisation strategy for the retirement of the owner and was done well before the idea of paying a dividend to the Trust and that the dividend being distributed to the owner was even considered.

The Court also found that the relevant dealing between the trustee and owner was an ordinary family or commercial dealing.

So if the Commissioner is ready to limit what is a family dealing, he is going to have to appeal this case and win.

Leave a comment