Have you ever heard of section 100A in the 1936 Act? This section allows the Commissioner to ignore any present entitlement you created and tax the trustee at the highest marginal rate. So when can the Commissioner do this? Where a beneficiary’s present entitlement to a share of trust income arises out of, or in connection with, an arrangement:

- Involving a benefit being provided to another person

- Intended to have the result of reducing someone’s tax liability, and

- Entered into outside the course of ordinary family or commercial dealing.

These are commonly called reimbursement agreements.

So the Commissioner has just released draft Practical Compliance Guideline PCG 2022/D1 Section 100A reimbursement agreements – ATO compliance approach . This draft Guideline sets out how the ATO differentiates risk for a range of trust arrangements to which he thinks section 100A might apply.

This is in addition to a draft Ruling on 100A and a Taxpayer Alert, which I have discussed before

But note that the Commissioner states that he won’t be looking at anything before 1 July 2014 due to this being when he published some previous guidance… but I doubt he is going to come looking at 2015 arrangements.

What does the Commissioner say we can do (he actually says he won’t undertake compliance activities in relation to section 100A)?

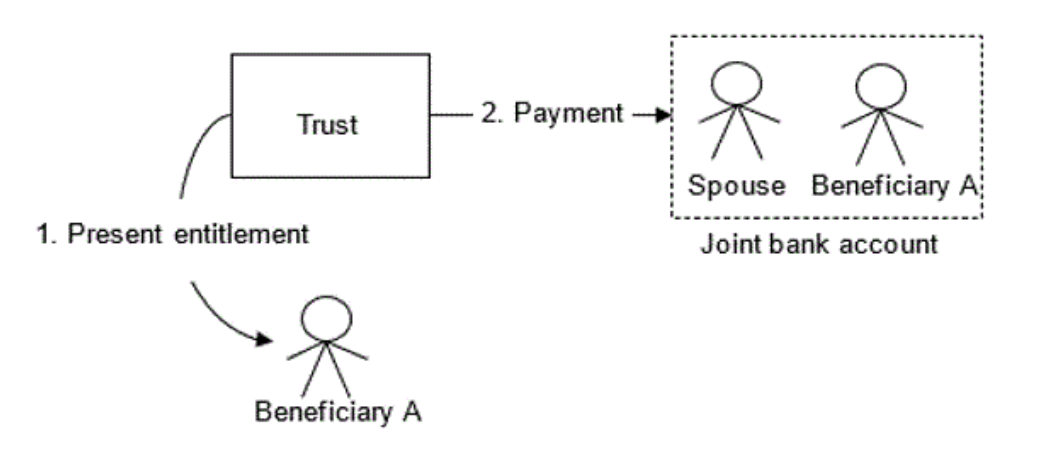

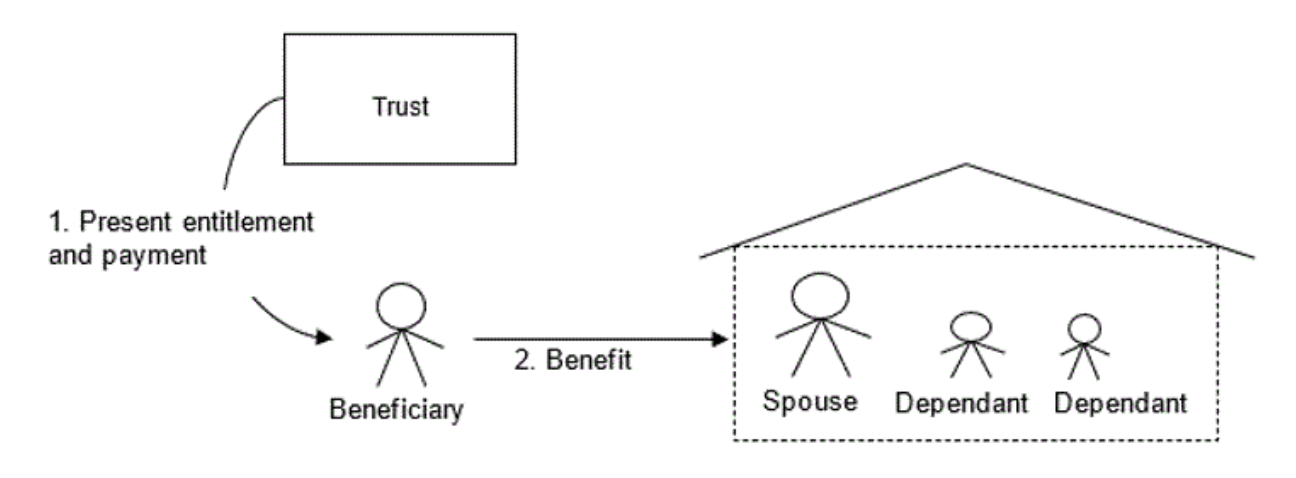

- An individual beneficiary is made presently entitled to income of the trust estate and the funds paid to the beneficiary are mixed with their spouse’s funds (for example, paid to a joint bank account) or used for joint family purposes, and/or benefit a person who is a dependant of the beneficiary…. like these two images

- Arrangement would likely be entered into in the course of ordinary family or commercial dealing.

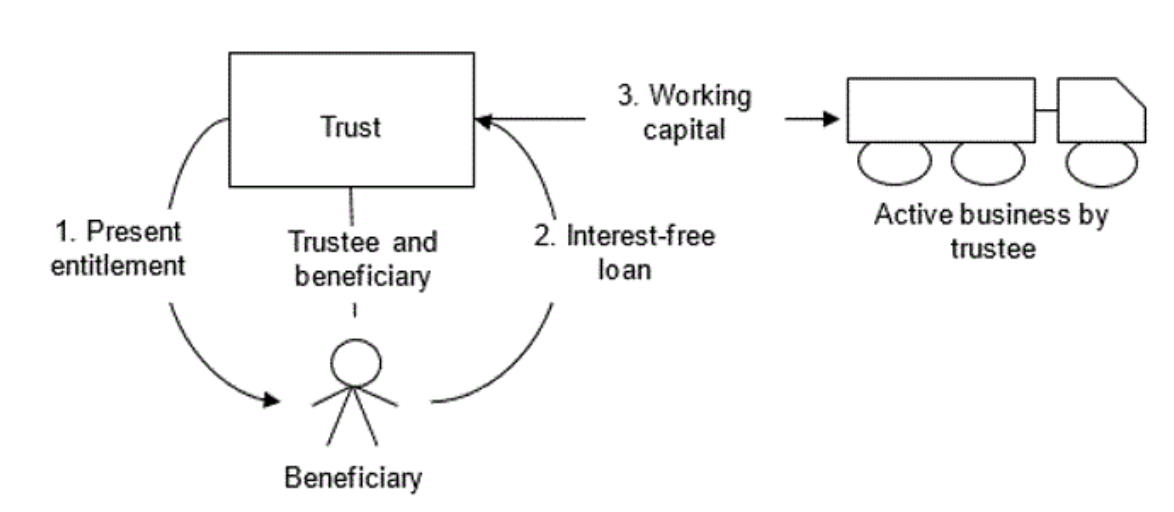

- A beneficiary that is an individual or a private company is made presently entitled to income of the trust estate and there is a ‘trustee retention of funds’, like these arrangements…

What does the Commissioner say we cannot do (he actually states he will undertake further analysis as a matter of priority in relation to section 100A)?

- Arrangements where the presently entitled beneficiary lends or gifts some or all of their entitlement to another party

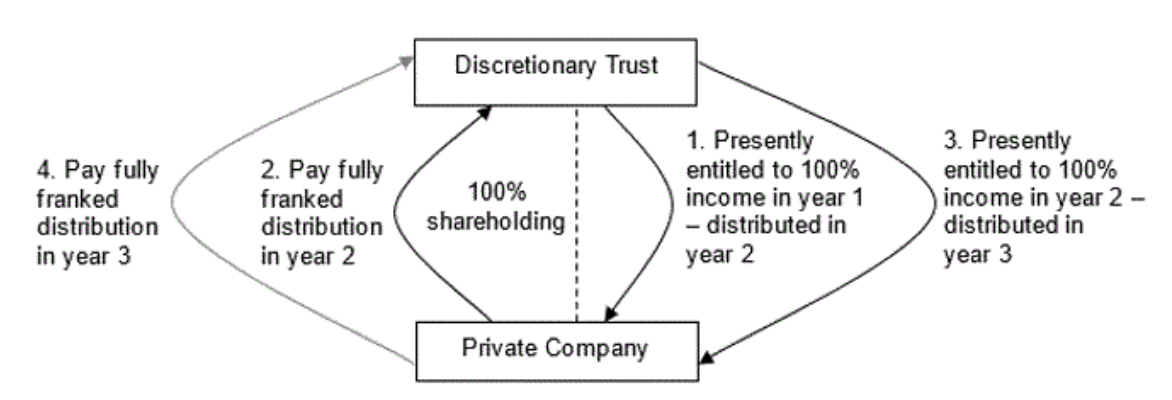

- Arrangements where trust income is returned to the trust by the beneficiary in the form of assessable income – the classic circular payments like this…

- Arrangements where the presently entitled beneficiary is issued units by the trustee (or related trust) and the amount owed for the units is set-off against the beneficiary’s entitlement

- Arrangements where the share of net income included in a beneficiary’s assessable income is significantly more than the beneficiary’s entitlement

- Arrangements where the presently entitled beneficiary has losses

- Arrangement where adult children just return their entitlement to their parents… This is the Taxpayer Alert I discussed in an earlier blog.

What does the Commissioner say falls between these two (he actually says he might undertake compliance activities in relation to section 100A but he does not know if he will yet)?

- The beneficiary makes a gift of their trust entitlement or an associated amount receivable from the trust

- The beneficiary disclaims their entitlement or forgives or releases the trustee from its obligation to pay their trust entitlement or an associated amount receivable from the trust.

- The income of the trust estate is less than the net income as a result of the trustee exercising a power, or the deed being amended, to affect the quantum of income of the trust estate.

- A beneficiary’s trust entitlement is satisfied by payments that are sourced from that beneficiary, or a beneficiary’s trust entitlement has been made subject to a loan agreement and the repayments of that loan are sourced from payments or loans from that beneficiary. Examples include

- where a dividend payable by a corporate beneficiary to the trustee is set-off against the amount payable by the trust

- where the trustee issues units in the trust to the beneficiary and the amount owed for the units is set-off against the amount payable by the trust, or

- where the trustee is made entitled to income of another trust that is comprised of franked distributions paid by the beneficiary.

So what does this mean? The Commissioner is going to make us think about who we make presently entitled and whether they get the actual distribution. We need to avoid the types of arrangements the Commissioner says are high risk – circular arrangements, issuing units, adult children, amending deeds, renouncing interests in trusts, … But everything is draft at the moment, so lets see what the finals look like.

Leave a comment